Jun 26, 2026Market Insights

2026 U.S. Pet Industry Trends Report: Market Set to Surpass $165 Billion

How the U.S. pet industry performed in 2025 and what growth brands can expect in 2026

The latest data released by the American Pet Products Association (APPA), together with insights from the 2026 State of the Industry Report, provides a clear picture of how the U.S. pet industry performed in 2025 and what growth brands can expect in 2026.

Despite ongoing economic pressure, the pet market continues to expand steadily. Pet ownership penetration is rising, generational dynamics are shifting, and consumer behavior is becoming more rational and necessity-driven.

1. Market Expansion Continues Year After Year

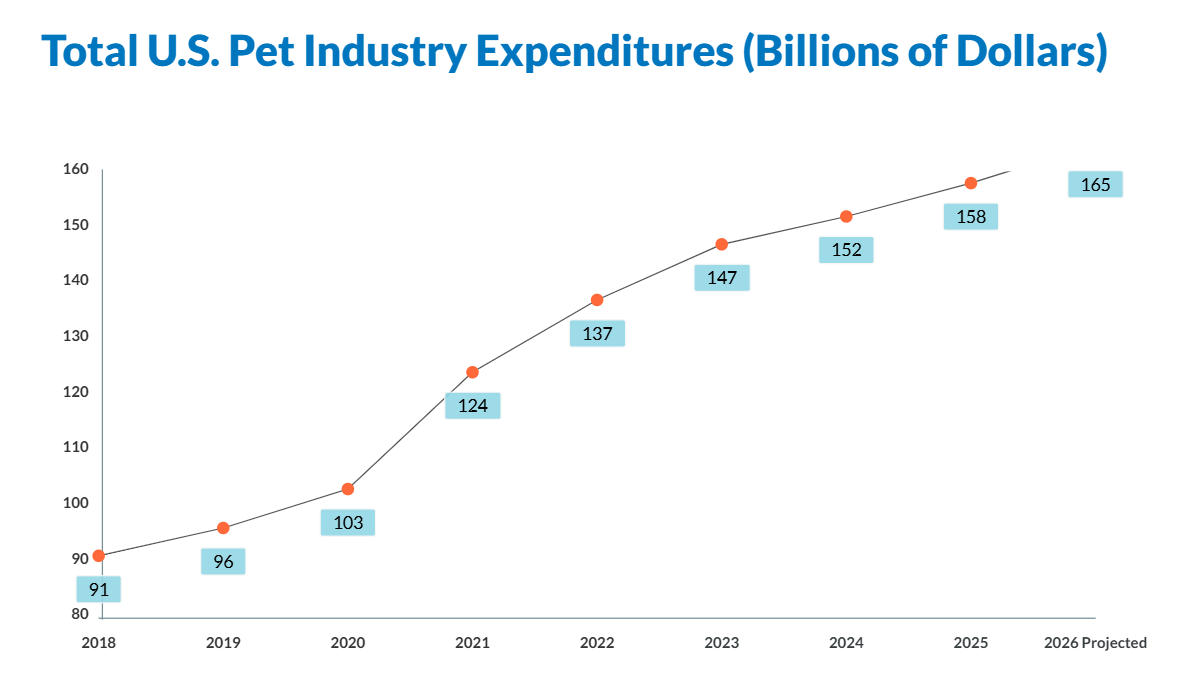

APPA’s newest figures show that the U.S. pet industry has maintained a long-term, stable growth trajectory. Spending has increased annually, demonstrating strong resilience even in uncertain economic conditions.

Market Size

- Total U.S. pet industry spending reached $151.9 billion in 2024.

- In 2025, actual spending climbed to $158 billion (approx. RMB 10930.28 billion), representing 3.7% year‑over‑year growth, slightly above the earlier forecast of $157 billion.

- For 2026, APPA projects the market will exceed $165 billion (approx. RMB 11415.69 billion), with an expected 4.4% annual growth rate, about 2 percentage points driven by inflation.

Growth Trajectory

From $90.5 billion in 2018 to $158 billion in 2025, the industry nearly doubled in seven years. Even during economic fluctuations, pet spending remained rigid, reinforcing the long-term trend of pets becoming full-fledged family members.

2. Four Major Spending Categories Remain Stable

U.S. pet spending is concentrated in four major categories. Pet food and veterinary care remain the two largest pillars, while supplies and services continue to grow steadily—together covering the full lifecycle needs of pets.

2025 Spending Breakdown

- Pet food & treats: $68.3 billion

- Supplies, live animals & OTC medications: $34.4 billion

- Veterinary care & product sales: $41 billion

- Other services (boarding, grooming, insurance, training, pet sitting, dog walking, etc.): $14.3 billion

2026 Forecast

- Pet food & treats: $69.7 billion

- Supplies, live animals & OTC medications: $35.6 billion

- Veterinary care & product sales: $42.4 billion

- Other services: $14.9 billion

Veterinary care stands out as the fastest-growing segment, signaling a shift from “basic feeding” to “health protection.” Meanwhile, food and treats remain the largest and most essential category—forming the industry’s foundation.

3. Pet Ownership Reaches New Highs

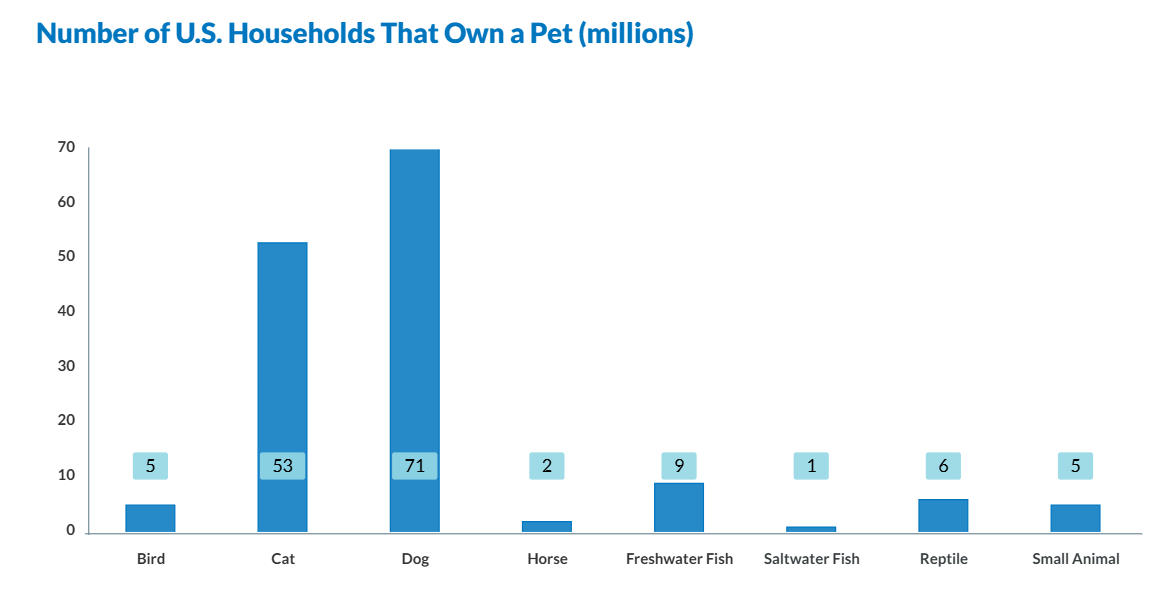

APPA’s 2026 report, based on the 2025 National Pet Owners Survey, shows that U.S. pet households increased from 94 million to 95 million, reinforcing pets as a standard part of American family life.

Household Pet Ownership

- Dogs: 71 million households (53% of U.S. households), adding ~4 million new homes

- Cats: 53 million households (39%), growing 5% year over year

- Birds, reptiles, small animals: 6 million households each

- Freshwater fish: 10 million households

- Horses & saltwater fish: 2 million households each

The dominance of dogs and cats remains strong, while niche pets maintain stable growth. Multi-pet households continue to rise, reflecting deeper emotional reliance on pet companionship.

4. Younger Generations Lead the Pet Economy

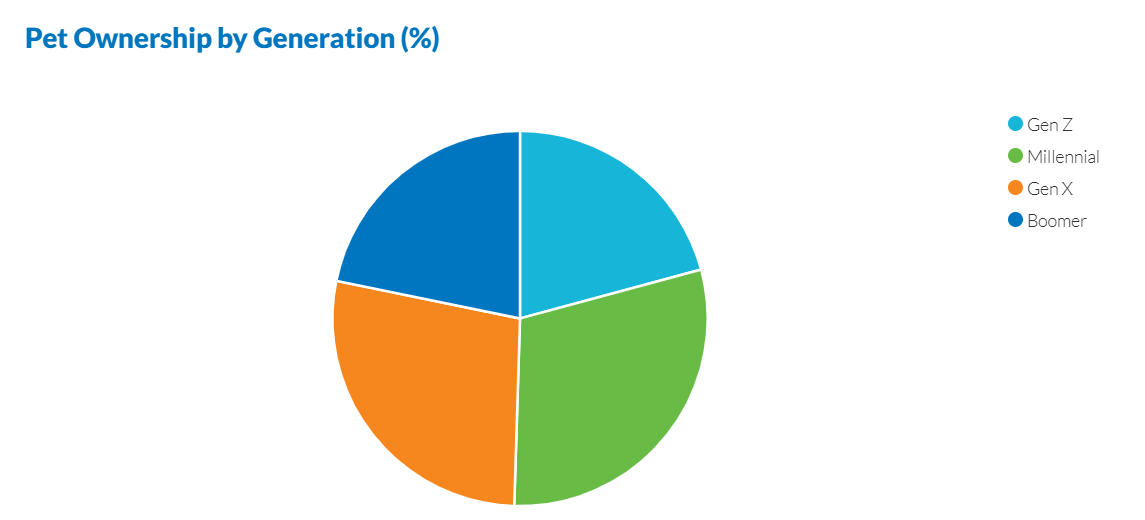

Generational shifts are reshaping the pet market, with distinct preferences and spending behaviors driving overall expansion.

Generational Breakdown

- Millennials: 30% (largest group)

- Gen Z: 20% (fastest-growing group)

- Gen X: 25%

- Baby Boomers: 25%

Generational Characteristics

- Gen Z + Millennials:

- Core drivers of dog and cat ownership

- Highly value emotional connection

- Willing to pay for personalized and health-focused products

- Least affected by economic pressure in pet-related decisions

- Gen X:

- Key growth engine in 2025

- Pet households grew 12%

- Strong expansion across categories: dogs +12%, cats +8%, birds +25%, reptiles +20%, freshwater fish +17%

- Exploring niche pet categories for new experiences

- Baby Boomers:

- More conservative and value-oriented

- Spending remains stable but grows slowly

5. Consumer Behavior Shifts Toward Rational Spending

Economic pressure is pushing U.S. pet owners to reallocate—not reduce—their pet budgets. Three major behavioral patterns have emerged:

1. Essential Spending Remains Protected

Around 50% of owners kept pet spending unchanged, prioritizing food and medical care even when tightening household budgets.

2. Rational Cutbacks Increase

22% of owners reduced pet spending, up 10 percentage points year over year, mainly cutting discretionary and non-essential purchases.

3. Spending Structure Optimizes

Consumers are shifting from premium treats and non-essential supplies toward basic care and health-related services. Value and necessity now outweigh impulse buying.

Pets have transitioned from “luxury companions” to “non-negotiable family expenses.” Owners adjust spending categories—not pet ownership itself—when facing economic uncertainty.

6. Three Key Trends Shaping 2026

1. Continued Market Expansion

Growth is expected to remain above 4%, supported by both inflation and real demand.

2. More Diverse Pet Owner Demographics

Growth is no longer driven solely by younger generations—Gen Z, Millennials, and Gen X are all contributing, while niche pet categories gain traction.

3. Increasing Category Specialization

Health care, functional nutrition, and essential services will continue to lead. Non-essential categories face restructuring, with value and professional quality becoming core differentiators.

Overall, the U.S. pet industry’s momentum is rooted in two forces: the humanization of pets and the essentialization of pet spending. As pets become indispensable family members, the industry gains long-term resilience.

For brands, the message is clear:

Winning the future requires anchoring in health, elevating service experience, and meeting the expectations of Millennial and Gen Z owners who demand scientific, refined pet care. This shift also increases the need for cost control, flexible production, and stable supply chains, especially for everyday functional products like harnesses, leashes, and recovery gear.

What This Means for the Pet Industry

- The U.S. pet market is entering a phase of steady, necessity-driven growth, supported by rising ownership and multi-pet households.

- Health-related categories—veterinary care, functional nutrition, and essential services—will continue to outperform.

- Generational diversification means brands must adapt to different expectations across Gen Z, Millennials, and Gen X.

- Value, functionality, and reliability will increasingly outweigh novelty or premium aesthetics.

What This Means for Pet Brands Working with OEM Partners

1. The Problems Brands Are Facing

- Rising costs are making it harder to maintain margins.

- Demand for functional, health-oriented products is increasing, requiring higher production consistency.

- Younger consumers expect better design, better fit, and better performance—especially in everyday gear like harnesses, leashes, and protective wear.

- Supply chain instability creates pressure to avoid stockouts and maintain product availability.

2. What Brands Now Need

- More cost-efficient manufacturing without compromising quality

- Flexible production capacity to respond to fast-changing demand

- Stable supply chains that reduce operational risk

- Faster development cycles to keep up with shifting consumer expectations

3. How OEM Partners Create Value

A strong OEM partner can support brands by providing:

- Cost control through optimized materials and scalable production

- Flexible manufacturing for both core SKUs and seasonal items

- Rapid prototyping to meet the expectations of Gen Z and Millennial buyers

- Reliable supply chain systems that ensure consistent delivery

This is especially relevant for functional #outdoorpetgear—harnesses, leashes, collars, recovery suits—where durability, safety, and fit directly influence customer satisfaction.