Jun 26, 2026Market Insights

2026 U.S. Private‑Label Pet Trends: Growth Momentum, Category Breakouts, and the Next Wave of Opportunities

The latest report from PLMA shows that in 2025, U.S. private label products achieved record highs in both sales and market share, even under economic pressure.

The Private Label Manufacturers Association (PLMA) has released its 2026 U.S. Private Label Report, revealing that private‑label products not only outperformed the broader retail market in 2025 but also reached historic highs in both sales and market share. Among all categories, pet care emerged as one of the strongest growth engines, driven by rising consumer trust, category innovation, and a shift toward more refined, value‑driven purchasing behavior.

From core categories like dog food and treats to fast‑emerging segments such as supplements and pet travel gear, private‑label pet products are evolving rapidly. The report highlights a clear trajectory: U.S. private‑label pet care is moving from basic value offerings toward premiumization, specialization, and functional differentiation—a shift that will shape the next decade of retail.

1. Private‑Label Pet Care Growth Performance

Leading Across the Board, With Emerging Segments Becoming Breakout Winners

In 2025, private‑label pet care outperformed nearly every major retail department. Whether measured by unit growth, dollar sales, or category expansion, pet care stood out as the “growth champion” within the private‑label ecosystem.

Department-Level Performance

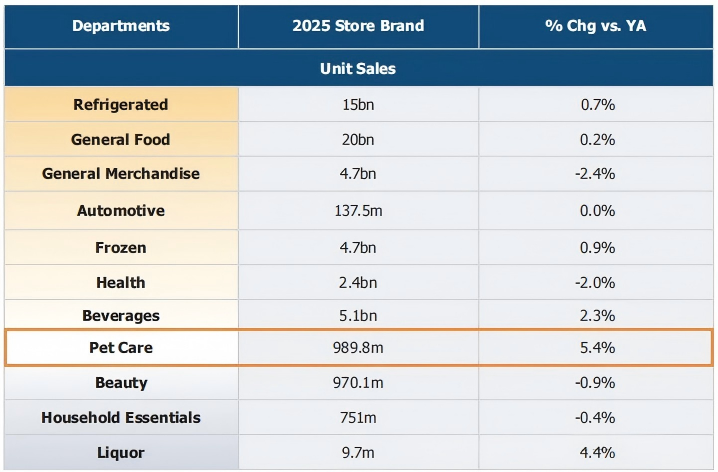

Pet care recorded the fastest unit sales growth among all private‑label departments in 2025:

- Unit sales: +5.4% (ahead of alcohol at +4.4% and beverages at +2.3%)

- Dollar sales: +3.7% (4th among all departments with positive growth)

By the end of 2025, private‑label pet care reached:

- $5.6 billion in dollar sales

- 989.8 million units sold

- 17.2% dollar share

- 18.1% unit share

This positions pet care as a core pillar within non‑food private‑label categories.

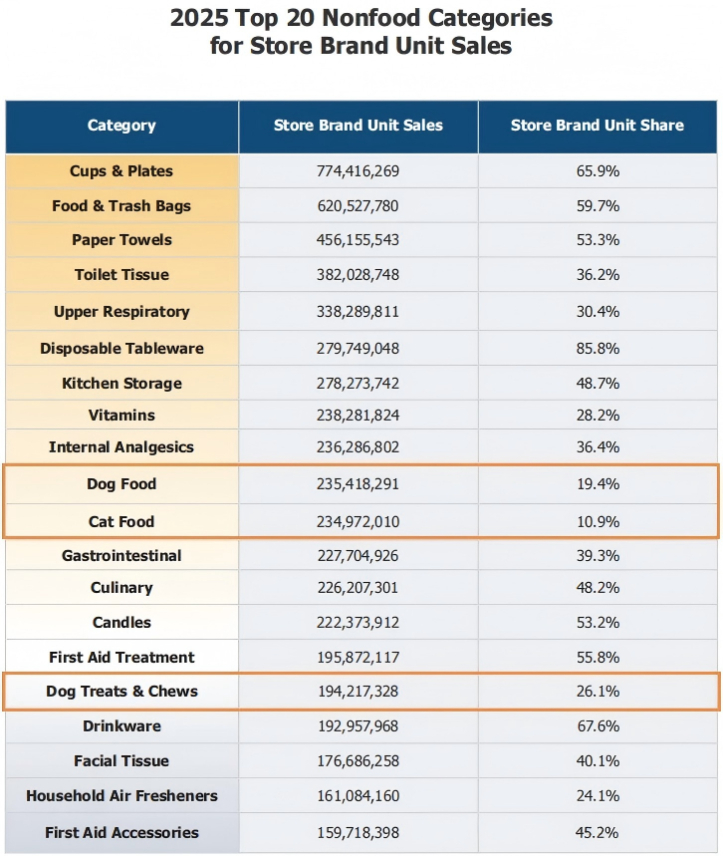

Core Categories: Dog Food and Dog Treats Lead the Pack

Pet categories dominate the non‑food private‑label Top 20 list, with dog food and dog treats serving as the primary drivers.

Dog food (private label):

- Dollar sales: $1.433 billion

- Dollar share: 13.3%

- Unit sales: 235 million

- Unit share: 19.4%

Dog treats & chews (private label):

- Dollar sales: $1.155 billion

- Dollar share: 23.1%

- Unit sales: 194 million

- Unit share: 26.1%

Cat food also gained momentum, with 235 million units sold and a 10.9% unit share, entering the Top 20 and becoming a new growth pillar.

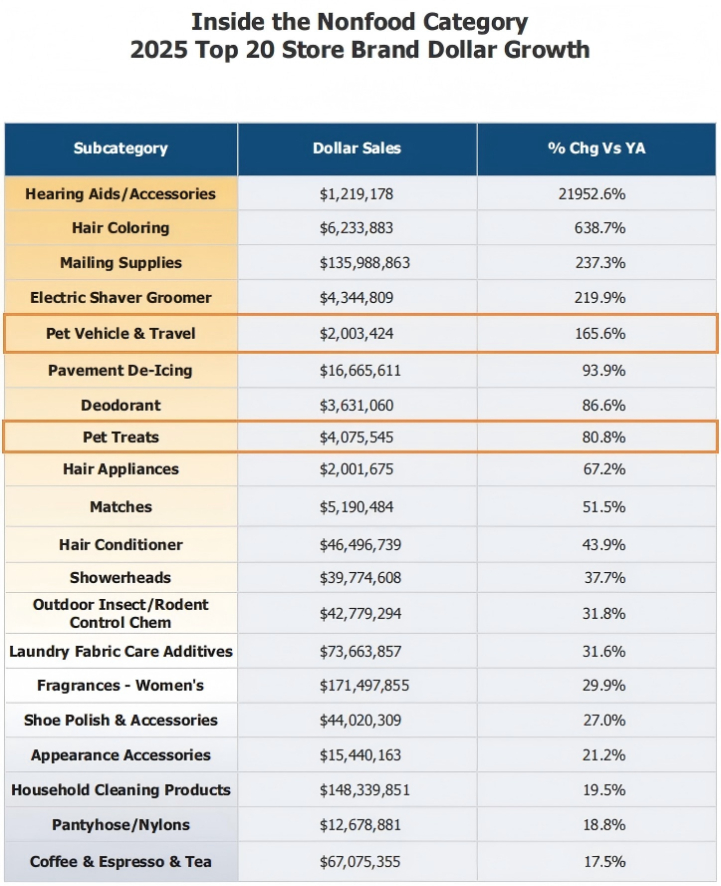

Emerging Subcategories: Explosive Growth Signals a New Wave

While core food and treat categories remain strong, emerging subcategories saw breakout growth in 2025:

- Pet strollers & travel gear:

- Dollar sales: +165.6%

- Unit sales: +130.4%

- Fastest‑growing subcategory overall

- Pet treats (emerging formats):

- Dollar sales: +80.8%

- Unit sales: +67.0%

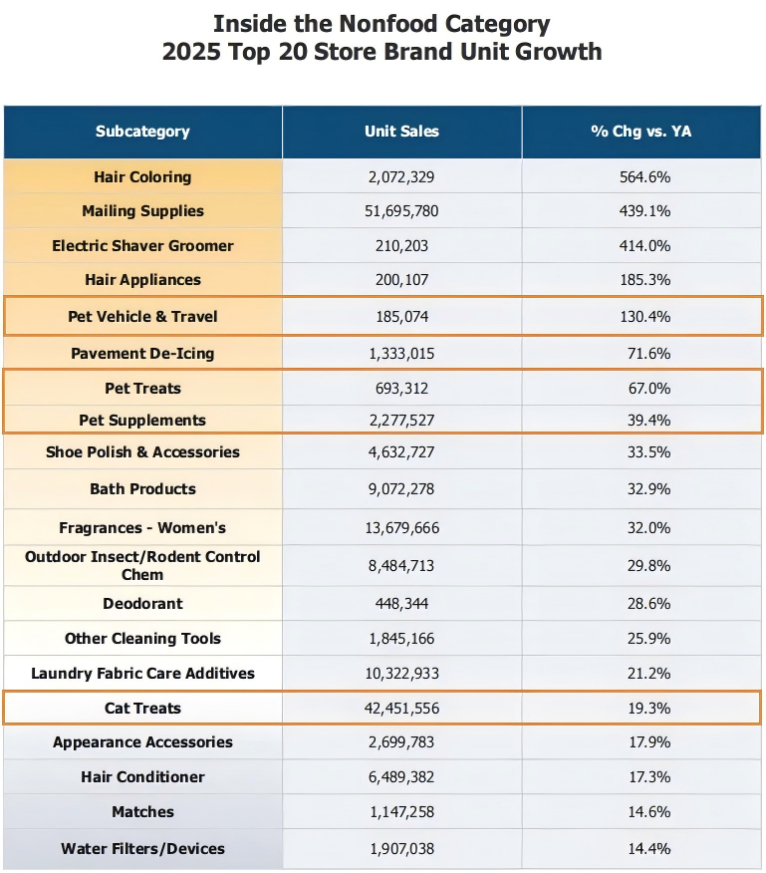

- Pet supplements:

- Unit sales: +39.4%

- Cat treats:

- Unit sales: +19.3%

These trends reflect a shift from “basic feeding” to specialized, functional, and lifestyle‑driven pet care, expanding the private‑label opportunity space—especially for functional outdoor gear such as harnesses, leashes, and travel accessories.

2. What’s Driving Private‑Label Pet Growth?

A Three‑Force Engine: Consumer Behavior, Retail Strategy, and Industry Maturity

The surge in U.S. private‑label pet care is not a temporary inflation‑driven phenomenon. It is the result of structural changes across consumers, retailers, and the broader industry ecosystem.

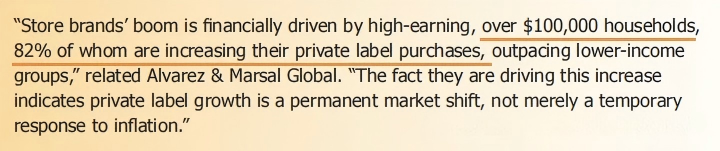

Consumer Drivers: High‑Income Households Lead the Shift

Contrary to the outdated perception that private label equals “budget only,” high‑income households are now the primary growth engine.

- 82% of households earning over $100,000 increased private‑label purchases in 2025

- This group represents the core of refined, premium pet spending

Consumer perception has fundamentally shifted:

- 80%+ believe private‑label pet food quality is equal or superior to national brands (McKinsey)

- 90% believe private label offers better value

- 59% trust private label due to retailer endorsement (NielsenIQ), especially Millennials and Gen Z

This trust is accelerating trial and adoption across pet categories.

Retail Drivers: Major Retailers Double Down

Leading U.S. retailers are using private label as a strategic differentiator—expanding assortments, upgrading branding, and investing in premium tiers.

Examples include:

- Costco’s Kirkland Signature: Pet products positioned as “same quality, 20% lower price,” contributing to one‑third of Costco’s revenue

- Walmart’s bettergoods: High‑end packaging and plant‑based/organic ingredients targeting affluent households, with pet categories upgrading alongside

- Kroger, Target, Amazon: Expanding Smart Way, Figmint, Saver, and other private‑label lines to strengthen pet offerings

Warehouse clubs and regional retailers are also launching niche and themed private‑label pet products, reinforcing differentiation.

Industry Drivers: A Mature Ecosystem Fuels Innovation

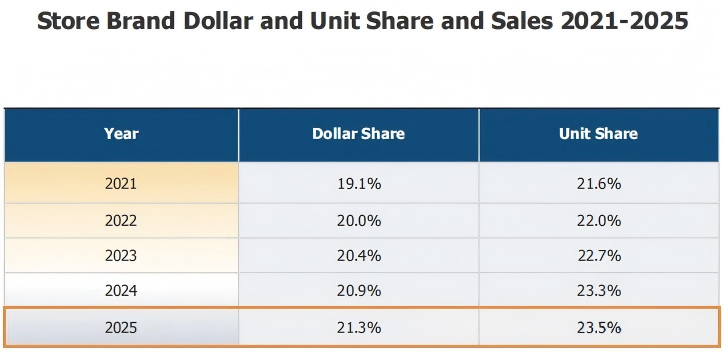

Private label reached 21.3% dollar share and 23.5% unit share in 2025—an all‑time high.

Innovation trends in plant‑based, functional, and sustainable products are now extending into pet care, including:

- Grain‑free formulas

- Probiotics

- Skin & coat functional diets

- Human‑grade ingredients

PLMA’s Chicago trade show in 2025 hosted 1,900+ exhibitors and 50,000+ products, with pet innovations gaining significant visibility.

3. Future Trends: From Scale Growth to Value Growth

Three Strategic Directions for the Next Stage of Private‑Label Pet Care

PLMA emphasizes that private‑label growth is a permanent structural shift, not a temporary inflation response. Pet care will now evolve from volume expansion to value‑driven, premium, and proprietary development.

1. Precision Segmentation

Emerging subcategories will continue expanding, addressing niche and specialized needs:

- Pet travel gear

- Nutritional supplements

- Oral care

- Customized grooming

- Breed‑, age‑, and size‑specific formulas

Retailers will increasingly fill gaps with targeted private‑label solutions.

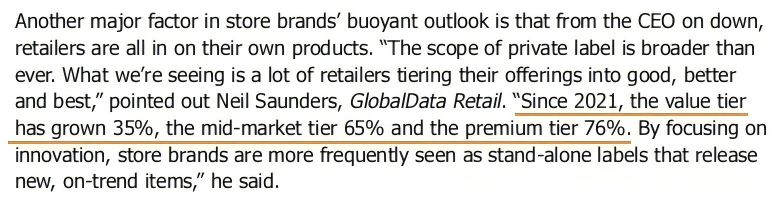

2. Premiumization (“Accessible Luxury”)

High‑income households will push private‑label pet care toward “value‑luxury,” driven by:

- Organic, grain‑free, human‑grade ingredients

- Functional benefits (low‑fat, hypoallergenic, digestive support)

- Elevated packaging and design

Since 2021, premium private‑label tiers have grown 76%, and pet care will follow the same trajectory.

3. Proprietary Product Development

The next evolution is exclusive, retailer‑owned pet products, including:

- Unique formulas

- Limited‑edition flavors

- Customized accessories

- Retailer‑exclusive gear

Retailers will differentiate through exclusivity, supported by deeper supplier collaboration.

Marketing & Supply Chain Enablement

- Social media and influencer partnerships will amplify private‑label pet brands

- Pet creators and pet influencers will drive content‑led discovery

- Retailers will integrate online and offline experiences

- Supply chain integration with OEM partners will ensure quality, cost control, and scalability

This creates strong opportunities for OEM/ODM manufacturers specializing in functional outdoor pet gear—harnesses, leashes, collars, recovery suits—where durability, safety, and design matter.

What This Means for the Pet Industry

- Private‑label pet care is entering a long‑term structural growth phase

- High‑income households are accelerating premium private‑label adoption

- Retailers are investing heavily in differentiation and exclusive product development

- Emerging subcategories—travel gear, supplements, functional treats—will reshape the market

- Innovation and supply chain excellence will determine competitive advantage

What This Means for Pet Brands Working with OEM Partners

1. The Problems Brands Are Facing

- Rising expectations for quality and functionality

- Pressure to offer premium features at accessible prices

- Need for exclusive, differentiated products

- Faster innovation cycles driven by retailer competition

2. What Pet Brands Now Need

- Cost‑efficient production to support value‑luxury positioning

- Flexible manufacturing for both core and emerging subcategories

- Rapid prototyping for exclusive and proprietary SKUs

- Stable supply chains to support high‑volume retail programs

3. How OEM Partners Create Value

OEM partners can accelerate private‑label pet growth by offering:

- Cost control through optimized materials and scalable production

- Flexible manufacturing for diverse product tiers

- Exclusive product development for retailer‑specific lines

- Reliable supply chain systems that ensure consistent quality and delivery

This is especially relevant for functional outdoor pet gear—harnesses, leashes, collars, recovery suits—where performance, durability, and design directly influence retailer adoption and consumer trust.